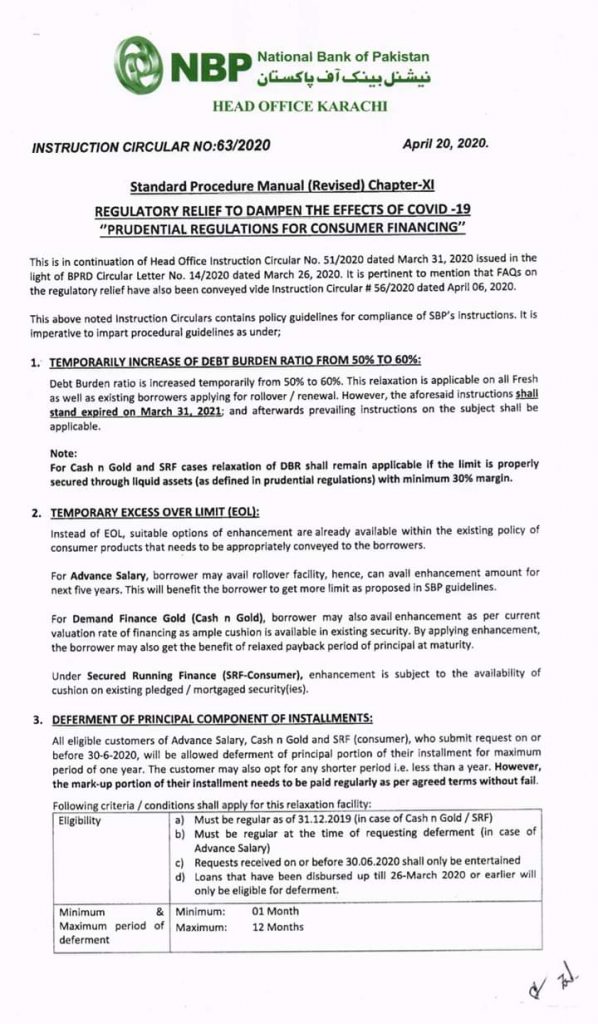

National Bank of Pakistan has issued the official Notification letter on 20th April, 2020 in connection with standard procedure manual (revised) chapter-XI, regulatory relief to dampen the effects of Covid-19 “NBP Prudential Regulations 2020”.

This is in continuation of Head Office Instruction Circular No. 51/2020 dated March 31, 2020 Issued in the light or BPRD Circular letter No. 14/2020 dated March 26. 2020. It Is pertinent to mention that FAQs on the regulatory relief have also been conveyed vide Instruction Circular # 56/2020 dated April 06, 2020.

This above noted Instruction Circulars contains policy guidelines for compliance of SBP’s Instructions. It is imperative to impart procedural guidelines as under;

Temporarily Increase of Debt Burden Ratio From 50% to 60%

Debt Burden ratio is Increased temporarily from 50% to 60%. This relaxation is applicable on all Fresh as well as existing borrowers applying for rollover / renewal. However. the aforesaid Instructions shall stand expired on March 31, 2021; and afterwards prevailing instructions on the subject shall be applicable.

Note:

For Cash n Gold and SRF cases relaxation of DBR shall remain applicable If the limit is properly secured through liquid assets (as defined In prudential regulations) with minimum 30% margin.

Temporary Excess Over Limit (EOL)

Instead of EOL, suitable options of enhancement are already available within the existing policy of consumer products that needs to be appropriately conveyed to the borrowers.

For Advance Salary, borrower may avail rollover facility. Hence, can avail enhancement amount tor next five years. This will benefit the borrower to gel more limit as proposed in SBP guidelines.

For Demand Finance Gold (Cash n Gold), borrower may also avail enhancement as per current valuation rate of financing as ample cushion is Available in existing security. By applying enhancement. the borrower may also get the benefit of relaxed payback period of principal at maturity.

Under Secured Running Finance (SRF-Consumer), enhancement is subject to the availability of cushion on existing pledged / mortgaged security(ies).

Deferment of Principal Component of Installments

All eligible customers of Advance Salary. Cash n Gold and SRF(consumer), who submit request on or before 30-6-2020, will be allowed deferment of principal portion of their installment for maximum period of one year. The customer may also opt for any shorter period i.e. less than a year. However, the mark-up portion of their Installment needs to be paid regularly as per agreed terms without fail.

Eligibility Criteria

|

Eligibility |

a) Must be regular as of 31-12-2019 (in case of Cash n Gold / SRF) b) Must be regular at the time of requesting deferment (In case of Advance Salary) c) Request received on or before 30.06.2020 shall only be entertained d) Loans that have been disbursed up till 26-March 2020 Or earlier will only be eligible for deferment |

|

Minimum & Maximum Period of deferment |

Minimum: 01 Month Maximum: 12 Months |